Intercompany errors are discrepancies in financial records between related entities, often caused by manual data entry, system differences, timing mismatches, or currency complications. These errors lead to inaccurate consolidated financials and compliance risks, requiring robust reconciliation processes to ensure accurate reporting.

Every CFO managing multi-entity operations knows the feeling. The close deadline looms, and your team discovers that Entity A's intercompany payable doesn't match Entity B's receivable. What should be a straightforward elimination becomes a days-long investigation, delaying consolidated reports and raising red flags with auditors.

These discrepancies aren't just annoying. They represent real business risk. Intercompany errors compromise the accuracy of your consolidated financial statements, create compliance vulnerabilities, and erode confidence among stakeholders who depend on timely, reliable reporting.

The good news? Understanding where these errors originate and how they manifest gives finance teams the foundation to prevent them. This post breaks down the root causes, explores the most common types of discrepancies, and offers practical strategies to eliminate errors before they derail your close.

What Are Intercompany Errors?

Intercompany errors are discrepancies that occur when transactions between related entities within the same corporate group don't reconcile. When Entity A records a sale to Entity B, both sides of that transaction must mirror each other perfectly. Entity A's revenue should match Entity B's expense. Entity A's receivable should match Entity B's payable.

The reciprocal nature of intercompany transactions makes them particularly vulnerable to error. Unlike external transactions where a single entity controls both sides of the entry, these transfers involve coordination between separate accounting teams, often working in different systems, time zones, and languages.

These errors matter because consolidated financial statements require the elimination of all enterprise activity. If the transactions don't match, the eliminations won't balance, and your consolidated financials will be inaccurate.

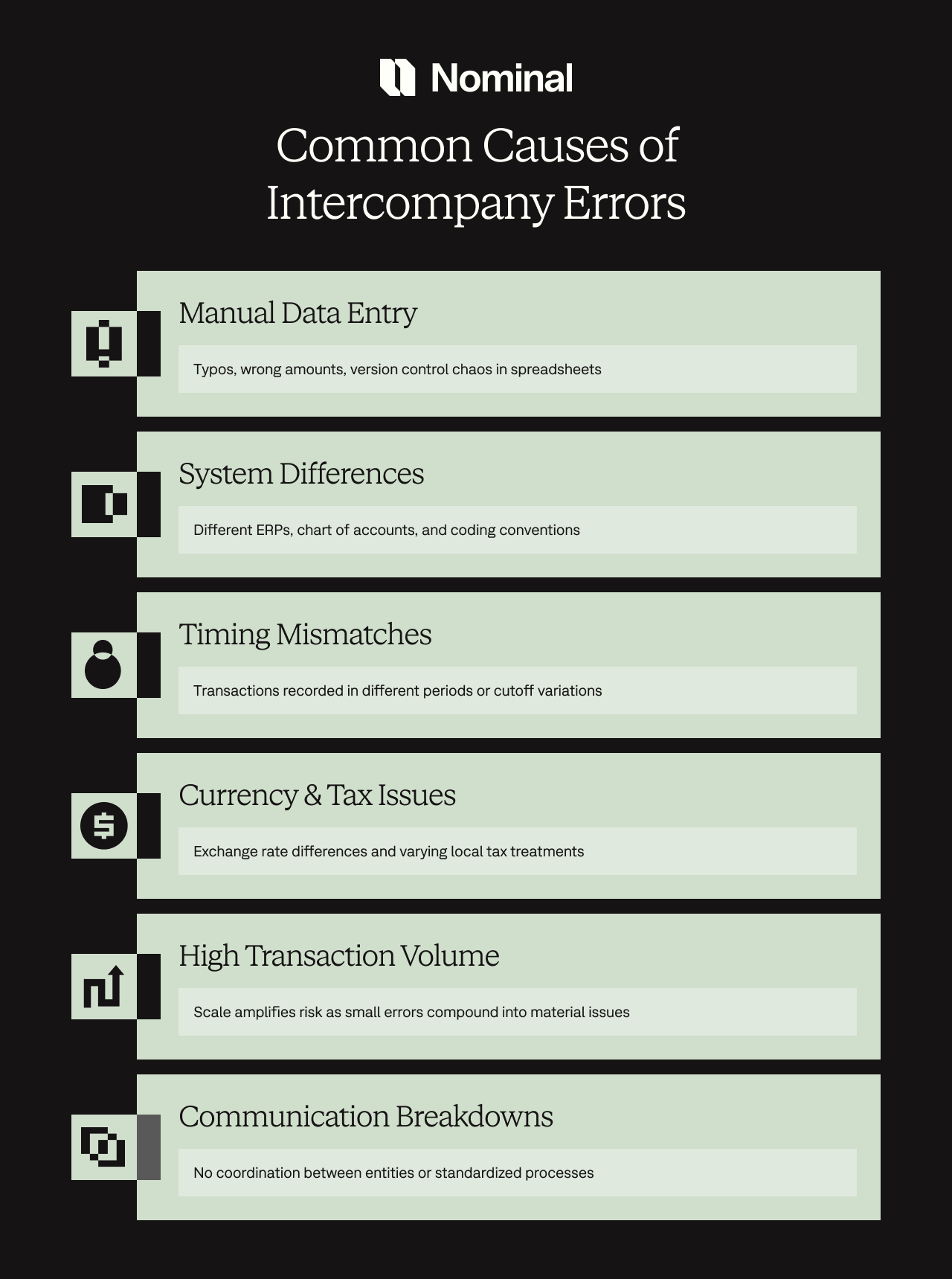

Common Causes of Intercompany Errors

Understanding why errors happen is the first step toward preventing them. Most discrepancies trace back to a handful of recurring root causes.

Manual Data Entry and Spreadsheet Dependence

The overwhelming majority of mistakes begin with manual data entry. When finance teams rely on spreadsheets to track intercompany activity, simple typos become inevitable. Someone enters $50,000 instead of $500,000. A transaction gets recorded at one entity but forgotten at another.

Spreadsheets create additional risk through version control chaos. Multiple people update different copies of the same file. By the time reconciliation begins, no one knows which version contains the correct data.

System and Process Differences

Multi-entity companies rarely operate on a single, unified ERP. Entity A uses NetSuite. Entity B uses SAP. Entity C still runs QuickBooks. Each system has its own chart of accounts, its own coding conventions, and its own definition of what constitutes an intercompany transaction.

These structural differences make matching transactions nearly impossible. One entity codes intercompany payables to account 2100. Another uses 2150. Without standardization, even accurately recorded transactions won't reconcile.

Timing Mismatches

Timing differences create some of the most frustrating reconciliation challenges. Entity A ships goods on December 31st and records the company sale in Q4. Entity B receives those goods on January 2nd and records the purchase in Q1. Both entries are technically correct, but they won't match during period-end elimination.

Cutoff procedures vary across entities. These inconsistencies compound during high-volume periods like quarter-end, when hundreds of transactions cross entity boundaries within days.

Currency and Tax Complications

Global operations introduce currency translation as another error vector. When Entity A in the US records a $100,000 transaction with Entity B in Europe, both entities must convert that amount to their functional currency. If they use different exchange rates or apply them at different times, the amounts won't match.

Local tax requirements add further complexity. Transfer pricing adjustments, VAT treatment, and withholding taxes all affect the recorded amounts. If these adjustments aren't communicated clearly between entities, reconciliation becomes a forensic exercise.

High Transaction Volume

Scale amplifies every other risk factor. A company with 50 intercompany transactions per month can probably track discrepancies manually. A company with 5,000 transactions faces exponentially greater risk. Small errors that would be immaterial in isolation compound into significant misstatements.

Communication Breakdowns

Perhaps the most overlooked cause of intercompany errors is a simple lack of communication. Entity controllers don't talk to each other regularly. There's no standardized process for confirming transaction details. Different people handle enterprise accounting at each location, with no central coordination.

When questions arise, email chains stretch across time zones and languages. Documentation is sparse or nonexistent. By the time someone identifies an error, the person who recorded it has moved to a different role.

Types of Intercompany Errors

Not all mistakes look the same. Understanding the taxonomy helps with both detection and resolution.

Data Entry Errors

The simplest errors are pure data entry mistakes. Someone types the wrong amount, selects the wrong account, or transposes digits. Entity A records $125,000 while Entity B records $152,000. These errors are usually easy to spot during reconciliation but time-consuming to research and correct.

More problematic are omissions, transactions recorded at one entity but completely missed at the counterparty. These create one-sided entries that throw elimination schedules completely out of balance.

Account Mismatches

Account mismatches occur when entities use different general ledger accounts for the same transaction. Entity A codes an intercompany management fee to account 6250. Entity B codes it to 6275. The amounts match, but the classification doesn't, creating problems for consolidated reporting.

Balance Mismatches

Balance mismatches represent the most common reconciliation headache. Intercompany payables and receivables should net to zero across the group. When they don't, it indicates transactions recorded at different amounts, missed entries, or timing differences that haven't been resolved.

These discrepancies often accumulate over time. Small differences in one period carry forward and compound in subsequent periods, making it increasingly difficult to identify the original error.

Unrealized Profit Errors

When entities sell inventory to each other, generally accepted accounting principles require eliminating any unrealized profit on goods still held within the corporate group. Errors occur when finance teams fail to identify company inventory, apply incorrect markup rates, or miss elimination entries entirely.

Classification Errors

Classification errors happen when transactions get categorized incorrectly. An intercompany loan gets recorded as an operating activity. Revenue transactions get coded as balance sheet movements. These errors might not create reconciliation differences, but they misstate the nature of consolidated activity.

Explore more on this topic: The Transaction Patrol Agent: How Finance Teams Automate Error Detection

The Real Cost of Intercompany Errors

The impact of mistakes extends far beyond accounting headaches. Delayed financial closes mean stakeholders wait days or weeks longer for consolidated results. Management can't make timely decisions. Board meetings get postponed.

Auditors view intercompany errors as control deficiencies. Material weaknesses in accounting can trigger qualified opinions, increase audit fees, and damage relationships with audit committees. Public companies face additional scrutiny from regulators.

The hidden cost appears in finance team morale. Month after month of reconciliation fire drills leads to burnout. Talented finance professionals spend their time hunting for discrepancies instead of providing strategic insights.

How to Prevent and Resolve Intercompany Errors

Prevention beats correction every time. The most effective strategies attack root causes rather than symptoms.

Standardize Processes and Documentation

Create written intercompany transaction policies that every entity follows. Standardize your chart of accounts across all entities, or at minimum, create clear mapping rules. Implement approval workflows that require both sides of a company transaction to confirm details before recording.

Use unique transaction identifiers that both entities reference. When Entity A creates intercompany invoice IC-2024-001, Entity B should record that same identifier. This simple practice eliminates guesswork during reconciliation.

Implement Regular Reconciliation Cadence

Don't wait until quarter-end to reconcile intercompany accounts. Monthly reconciliation catches errors while they're still fresh and easier to research. Some high-volume organizations reconcile weekly or even daily.

Assign clear ownership to each entity. Someone needs to be accountable for timely, accurate multi-entity accounting. Set firm deadlines and escalate when entities miss them.

You might also like: What Is Month-End Flux? How Finance Teams Analyze Variances Faster

Improve Communication Between Entities

Establish an intercompany coordinator role at each entity. Hold regular meetings where coordinators discuss upcoming transactions, resolve open items, and share process improvements. Create shared documentation repositories where both parties can access supporting information.

Standardized templates for transaction confirmations eliminate ambiguity. When Entity A sends an intercompany invoice, Entity B should receive enough detail to record their side accurately.

Leverage Technology and Automation

Manual processes and fragmented systems make errors inevitable at scale. Modern accounting platforms can automate multi-entity matching, flagging discrepancies instantly rather than weeks after transactions occur. Real-time visibility across all entities means controllers can spot and resolve issues before the period close.

Automated elimination entries remove another source of manual error. The system calculates what needs to be eliminated based on actual recorded transactions, ensuring consolidated financials accurately reflect the economic substance of the business.

Moving Toward Error-Free Intercompany Accounting

Intercompany errors represent more than accounting inconvenience. They signal fundamental weaknesses in financial processes and controls. As companies grow more complex, with more entities, more transactions, and more geographic spread, the manual approaches that worked for smaller organizations break down entirely.

The path forward combines standardization, accountability, and automation. Finance leaders who audit their current processes honestly, invest in proper controls, and leverage technology to eliminate manual work will find their teams spend less time fighting fires and more time providing strategic value.

Ready to eliminate intercompany errors and close faster? See how Nominal automates reconciliation and eliminations for multi-entity finance teams. Book a demo today.