Flux analysis is the process of identifying and explaining significant changes in financial account balances across periods. Accounting teams use it during the month-end cycle to detect errors, satisfy audit requirements, and give leadership context behind performance shifts. When powered by AI, the process moves from hours of manual investigation to minutes of focused review.

Every Controller knows the moment. The preliminary financials come in, you scan the P&L, and something stops you. Revenue is up 18%, but the sales team did not flag a major deal. Marketing spend dropped when the campaign was supposed to be ramping up. Legal expenses spiked with no obvious explanation.

These are not anomalies to ignore. They are signals that demand investigation. And investigating them thoroughly, documenting the findings clearly, and delivering explanations that satisfy auditors, executives, and board members is one of the most important responsibilities in the entire month-end cycle.

This is flux analysis. For accounting teams managing multi-entity operations, it is also one of the greatest opportunities to move faster, stay audit-ready, and deliver the kind of insight that earns a seat at the leadership table. Understanding what drives variances, how the analysis process works, and where intelligent automation is taking it is essential for any Controller or accounting leader building a modern, scalable operation.

Watch our walkthrough in this episode of the Bottom Lines to see how Nominal automates flux review in real time.

What Is Flux Analysis in Accounting?

Flux analysis, also called fluctuation analysis, is the process of identifying and explaining material changes in account balances over time. Accounting teams typically compare results across periods, current month versus prior month, current quarter versus prior quarter, or actual versus budget, and investigate any variance that exceeds a defined materiality threshold.

The goal is not simply to confirm that numbers changed. It is to understand why they changed, whether the change reflects real business activity or a recording error, and what the change means for reporting accuracy and forward-looking decisions.

Done well, flux analysis produces financial statements that leadership can rely on, audit documentation that holds up under scrutiny, and operational insights that surface trends before they become strategic problems. It is where accounting work transitions from data maintenance to business intelligence.

What Causes Month-End Flux?

Variances emerge from multiple sources, and experienced Controllers learn to distinguish between routine fluctuations and items that require deeper investigation.

Timing Differences

Accruals that do not materialize as expected, revenue recognition adjustments, and period cut-off issues all generate variances. A large prepayment in one month creates a spike that reverses in the next. Quarter-end incentives concentrate expenses in specific periods that look unusual in isolation.

Volume and Business Changes

More customer invoices mean higher revenue. Seasonal hiring drives up payroll. A successful campaign generates increased spend alongside corresponding pipeline activity. These variances tell the story of business growth or contraction and are often the most straightforward to explain.

Operational and Pricing Changes

New product launches shift the cost structure. Pricing adjustments change revenue per transaction. Reorganizations move expenses between departments, creating apparent variances that are purely structural rather than operational.

System and Process Issues

Transactions coded to the wrong GL account require reclassification. Manual journal entries correct errors from automated processes. Multi-entity operations surface intercompany discrepancies that need resolution before consolidated financials can be finalized.

Helpful resource: Intercompany Accounting: How AI Agents Solve It at Scale

External Factors

Currency fluctuations affect companies with international operations. Market conditions impact investment valuations. These variances are real and often outside the team's control, but explaining them clearly and consistently is still a compliance requirement.

The important perspective shift here is that flux itself is not a problem to solve. It is information to interpret. Accounting teams that approach variance analysis as an intelligence function rather than a compliance checkbox consistently deliver more value to their organizations.

Why Flux Analysis Matters for Accounting Teams

Variance analysis serves multiple functions simultaneously, and each one contributes directly to the strategic value accounting teams deliver.

Audit Readiness Built Into the Workflow

Auditors expect accounting teams to understand their numbers at a detailed level. Teams that document variances consistently throughout the year enter audit season with complete, traceable records rather than reconstructing explanations under pressure. This is the difference between audit readiness as an outcome and audit readiness as a scramble.

Faster Data-to-Decision Making

When leadership reviews monthly results, the speed at which accounting can explain what changed determines how quickly the business can act on that information. Fluctuation analysis that takes days to complete delays every downstream decision. Teams that deliver clear, well-documented explanations alongside the financials compress the gap between data and action significantly.

Growing with a Lean Team

For accounting teams managing multiple entities, the volume of fluctuations that require investigation scales with the business. Manual processes require proportionally more headcount to keep pace. Accounting operations that embed this work into structured, repeatable workflows can absorb growth in transaction volume and entity count without adding headcount at the same rate.

Eliminating Dependence on Institutional Knowledge

In most accounting teams, flux analysis depends heavily on individual expertise. The Controller knows that a spike in professional services fees always coincides with the annual insurance renewal. The senior accountant who remembers that a specific entity runs payroll a week late every December. When those individuals leave, that knowledge leaves with them.

For accounting teams managing multiple entities, the volume of fluctuations that require investigation scales with the business. Manual processes require proportionally more headcount to keep pace. Accounting operations that embed this work into structured, repeatable workflows can absorb growth in transaction volume and entity count without adding headcount at the same rate.

The Traditional Approach and Its Limits

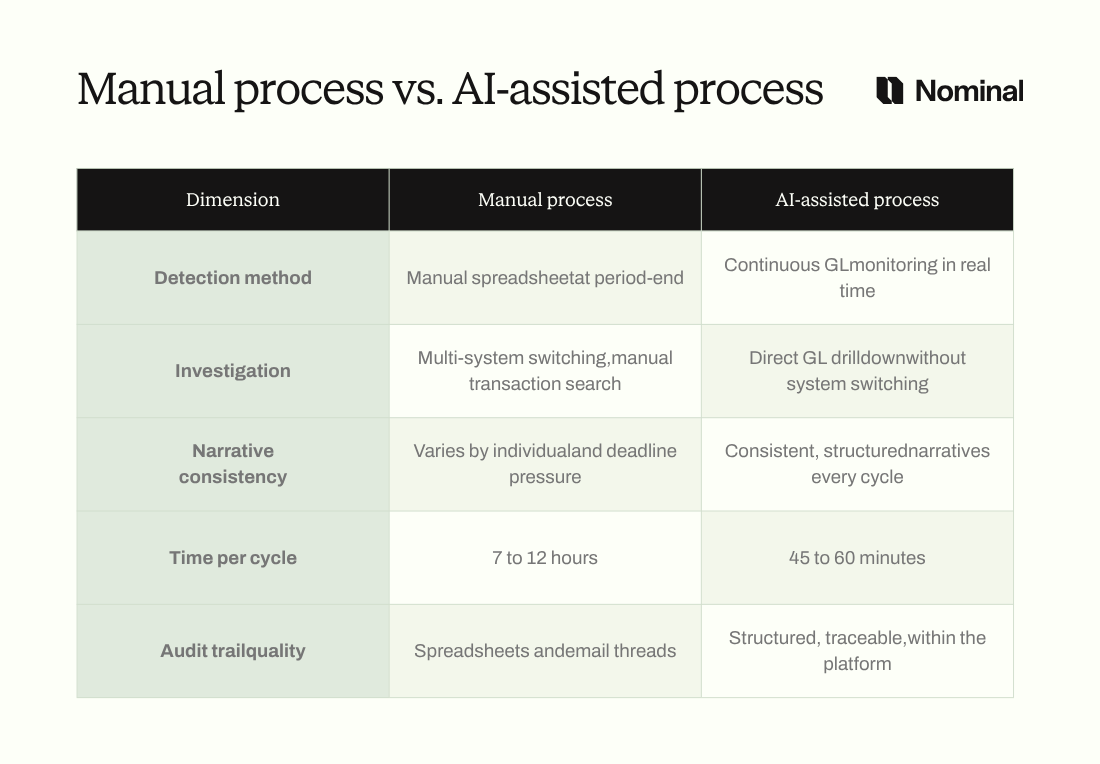

Despite advances in accounting technology, most teams still rely on a manual process built around spreadsheet exports, period-over-period calculations, and hand-written narratives.

The workflow starts with pulling trial balance data from the ERP into a workbook. Teams calculate changes across hundreds of GL accounts, apply materiality thresholds, and then drill into flagged items by reviewing individual journal entries and transaction details across multiple systems. Once the investigation is complete, someone writes narrative explanations for each material change, targeting an audience that ranges from auditors to board members.

Leadership reviews the commentary, requests revisions, and the cycle repeats. Total time: seven to twelve hours per period-end cycle, at the point in the month when the accounting team's capacity is already stretched across reconciliations, journal entries, and reporting.

The deeper issue is structural. Manual flux analysis produces output quality that varies with the individual handling it each cycle. It generates documentation that lives in spreadsheets and email threads rather than a traceable record. And it depends on the institutional knowledge of specific team members rather than a system that retains and applies that context consistently.

How AI Is Changing Flux Analysis

Modern accounting platforms built on Agentic Performance Management are transforming variance analysis by automating the mechanical work while keeping accounting judgment firmly in the loop.

Continuous Variance Detection

Rather than waiting until period-end to calculate changes in spreadsheets, intelligent systems monitor GL data continuously and flag material fluctuations based on configurable thresholds. Accounting teams gain visibility into emerging movements throughout the month, which means issues surface earlier and the period-end cycle starts with fewer surprises.

Related post: How APM Transforms Close Management from Coordination to Execution

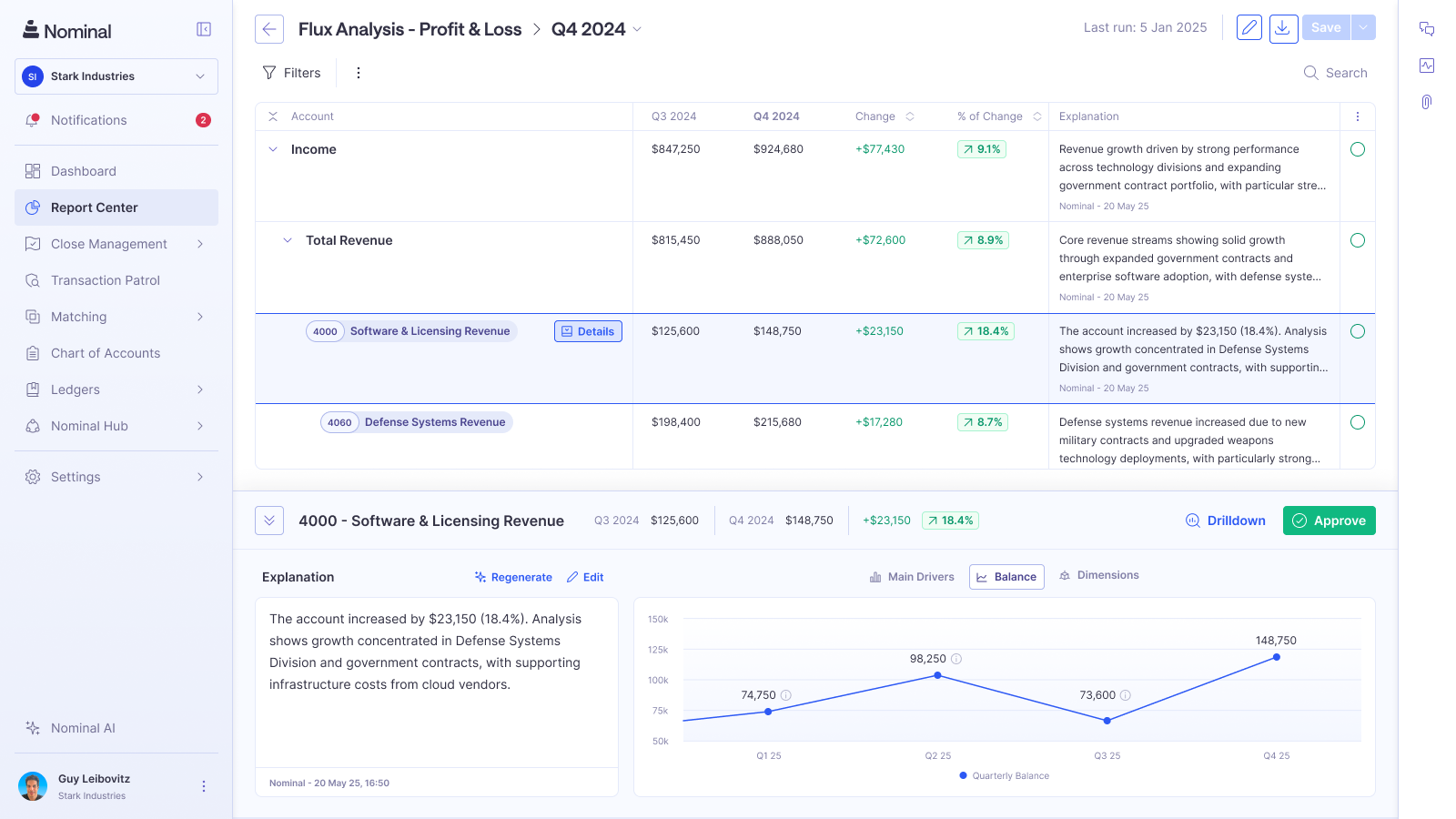

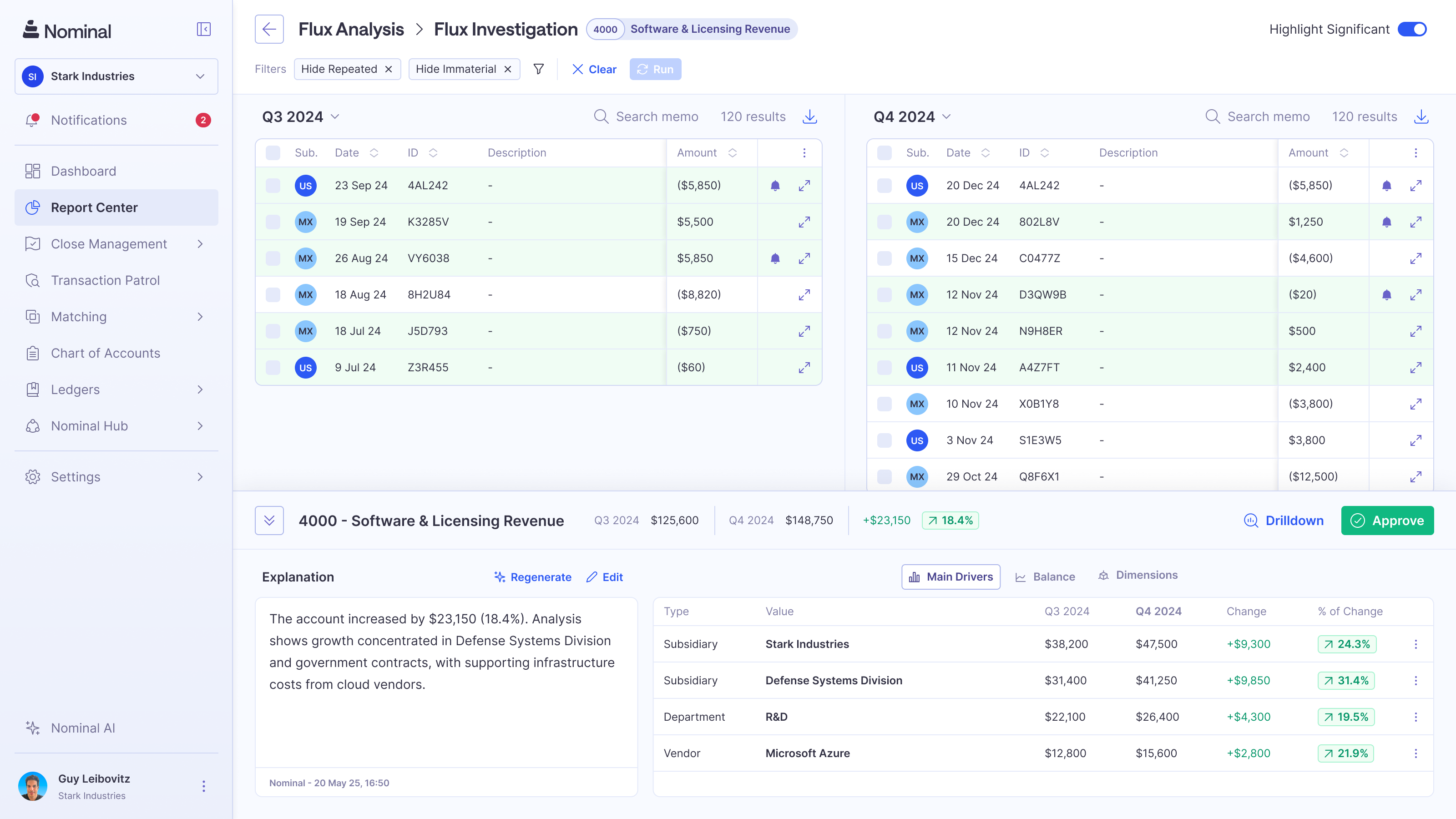

GL-Level Investigation Without System Switching

When a fluctuation appears, accountants can drill directly into the journal entries and transaction details that drove the change, without switching between systems or rebuilding context from scratch. Instead of a narrative that says legal expenses increased, the explanation can cite the specific invoices: a trademark filing, a litigation support engagement, and a contract review. That precision is what auditors require and what leadership trusts.

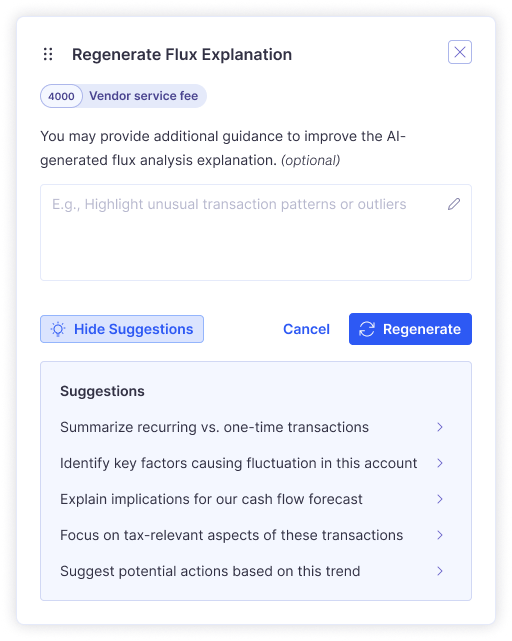

AI-Generated Narratives Backed by Transaction Data

The most significant shift is AI that produces plain-language variance explanations grounded in actual GL data. Accounting teams receive draft narratives that identify what changed, quantify the impact, and reference the specific entries that drove the movement. Narrative quality is consistent regardless of who runs the analysis or how much deadline pressure the team is under.

This directly addresses the institutional knowledge problem. The system does not rely on one person's memory of last quarter's anomalies. It applies context from historical patterns and transaction-level data every cycle, consistently.

Explore more on this topic: What Are Flux Agents? AI-Powered Variance Analysis for Finance Teams

Accounting Judgment Remains Central

This model works because human oversight is built into every step. Accountants review generated narratives, add business context the system cannot infer, refine explanations through feedback, and approve final commentary before it reaches any stakeholder. The agent handles the investigation and drafting. The Controller governs the output.

This is the Agentic Performance Management approach: agents execute the accounting work, humans provide strategic oversight. Applied to flux analysis, accounting teams that previously spent eight to twelve hours per cycle on variance review complete the same work in under an hour, with more consistent documentation and a stronger audit trail.

Best Practices for Flux Analysis

These principles apply whether teams are running manual processes today or transitioning to intelligent automation.

Combine percentage and absolute dollar thresholds

A 50% change in a minor account may be less significant than a 5% movement in a high-volume GL account. Thresholds that account for both dimensions prevent teams from investigating noise while missing material items.

Build a library of recurring drivers

Every accounting operation has predictable movement patterns tied to normal business activity. Quarter-end sales incentives, seasonal payroll fluctuations, and annual contract renewals appear reliably in specific periods. Documenting these recurring drivers reduces investigation time and produces more consistent narratives cycle over cycle.

Allocate dedicated investigation time in the month-end schedule

Variance analysis compressed into the final hours of the close consistently produces weaker documentation. Teams that protect time for flux review earlier in the cycle produce better output and catch issues while there is still time to resolve them.

Connect variance insights to forward-looking guidance

The accounting teams that earn the most influence with leadership are the ones that go beyond explaining what happened and surface what it implies. A change driven by accelerating customer acquisition costs is not just a historical data point. It is an input for the next forecast revision.

From Compliance Task to Strategic Advantage

Flux analysis will always require accounting judgment. The numbers tell only part of the story, and experienced accountants provide the business context that transforms raw variance data into actionable insight. But the mechanical work of calculating changes, investigating journal entries, and producing first-draft narratives belongs in an automated workflow, not on a spreadsheet.

Accounting teams that make this shift do not lose their role in the process. They gain the capacity to focus on the judgment work that actually differentiates a high-performing accounting function. Faster explanations. Stronger audit documentation. Institutional knowledge that stays in the system when team members move on.

That is what modern flux analysis looks like, and it is available now.

Want to see how Nominal's Flux Agent automates variance detection and narrative generation? Book a demo to see how it fits into your period-end workflow.

.png)